The BIS described the 2008 crisis as a dollar shortage. I believe evidences from around the world are clearly indicating that the great dollar shortage is back.

This is a 40 year deflationary trend of the global reserve currency that has already negatively impacted global GDP growth, with each debt contraction increasing in severity.

Deflation is the predominant cause of depressions. With debt and malinvestment at record highs, the ending of debt ponzis around the world could have greater consequences than the previous debt contractions, including 2008.

Mexican Peso Crisis

In 1994 Mexico was needing to use their dollar reserves in the open market to buy back pesos to “maintain” the value of the peso. Turns out a central bank telling the market the rate at which it will buy back an asset doesn’t “control” that rate. The peso slid down, well below their declared peg.

Think of a currency peg like corporate share repurchases, where they buy their own stock to retire it and increase the value per share. However, the value of a share price will still be dictated by the cash the company outputs. Yes, the number of shares matters, but it is the denominator of value — i.e. value is the cash the company creates.

Similarly, a currency and central bank are valued by the productivity of the economy and reserves, and the currency is the denominator.

Many central bankers around the world still seem to believe that you can save a country’s currency based on the denominator alone, just like an indebted company (like GE or Boeing) thinks they can borrow (at the cost of productivity) to boost their share prices as their earnings decline. It never works. Value comes from future cash flows.

If a central bank has enough reserves and cash flow to buy back 100% of its notes then it could in theory control the price of the currency. But markets are self-correcting, so in reality, that would just mean the value of the currency goes up. Similarly, if a company has enough cash to buy back all its shares, the value of the company should and will be higher. The market discovers all rates for all assets, central banks do not set or control them.

As Mexico’s deficit grew, reserves dwindled and their dollar denominated debt obligations increased. As Mexico was using their dollar denominated reserves for debt payments they had fewer dollars for buying back pesos. It’s often retold as Mexico “choosing” to decrease the value of the Peso, but clearly the market value was lower without their buying pesos and they ran out of dollars to buy it back. What choice did they have?

The US then lent Mexico 20 billion dollars (a lot for the time) and helped raise a total of $50 billion just to “maintain” the new “peg”. It didn’t work either. Like the central banker economists they are, they thought the problem with the pesos’ value could be solved with increased “confidence”. However, markets don’t set rates based on faith or confidence in the long run, as commonly believed, but arbitrage does — supply / demand.

Like a stock declining when the cash flows of the underlying business is declining, no amount of share repurchases increase the company value — currencies are valued by the market based on the productivity of the economy. Mexico’s taxpayers took on a long term debt burden in appreciating dollars and wasted that money on pesos which depreciated anyway. A bad combo — appreciating liabilities, depreciating assets.

Pegs turn into ponzis. If countries can’t produce surplus then the value of a currency declines and the only way to maintain the peg is with debt. But then the country has more dollar debt obligations, larger interest payments, and thus will eventually need more debt to make the payments and to maintain the peg.

Sri Lanka has the same story but with a less powerful neighbor and, unfortunately, a smaller position in the global economy.

What really makes the situation worse is that virtually all global trade is conducted in dollars (or dollar denominated assets — “EuroDollars”) and the dollar has been going up in value for decades. In other words, debts get heavier. Central banks around the world have dollar reserves similar to how we have gold reserves (and somewhat similar to our oil reserves). They both serve as backing for their currency and as an emergency source to pay for imports.

As Sri Lanka runs out of dollars their purchasing power and ability to import essential goods decreases.

We’re All Island Economies Now

My wife and I started the year in a remote airbnb in Jamaica. Being remote, we cooked for ourselves for the two weeks, and in the grocery stores I began to notice something I would then notice all over the world, as our travels continued.

In these grocery stores there were very few things made in Jamaica. Almost everything was an American brand — Colgate toothpaste, Quaker oats, Oreos, Pepsi, cleaning supplies… Almost everything except meat and the limited fruits and vegetables.

As our travels continued across other continents, I saw it everywhere — shoes, smart phones, cars, oil — it’s all imported.

Consider all the items essential to Sri Lanka and Jamaica, and then consider how many they can provide for themselves. Even large amounts of food are imported to these islands. Sri Lanka imports billions of dollars of food and has less than $2 billion in reserves.

Sri Lanka’s Dollar Shortage Crisis

We were in Sri Lanka in early March when the rupee started declining.

The Sri Lankan rupee is “pegged” so it’s believed that central bankers chose the price of the rupee (which is like saying Apple chooses the price of their stock). Central bankers believe that if you tell the market how much you’ll pay for an asset, the market will value that asset accordingly — (the US lent to Mexico to maintain “confidence”, but the market works on arbitrage, not confidence or on central banks’ declared values). Sri Lanka, like Mexico, simply ran out of reserves to maintain the “peg” and the value of the rupee declined.

The thing to emphasize here is that if a country can produce excess reserves via GDP growth, it doesn’t need a peg. If a peg is maintained because GDP growth is declining, and therefore the currency would decline, then a peg is a ponzi. That is, if you can’t sustain the peg with cash flows (via tax), then you need more debt, and that’s just a debt ponzi.

Even before the depreciation of the rupee, reserve dollars were being drained on imports — something we’re seeing all over the world right now. Because they couldn’t import as much oil, they began to do rolling power outages. During our month-long stay the 2 hour outages became 10 hour power outages.

Diesel became incredibly scarce and the gas stations that had it would quickly get lines hundreds of cars long. I’ve really never seen anything like it. The line included cars, semi trucks and sections of pedestrians carrying 5 gallon gas jugs.

When Sri Lanka’s private sector stopped being productive enough to produce enough dollars to maintain imports and meet dollar bond obligations, the government stepped in and offered its dollar reserves for import, a source that was already depleting.

Like Mexico in ’94, Sri Lanka immediately went looking to India, China and the IMF for loans. Since bankers all over the world believe this recession is almost over, they cautiously extended small loans, which may have delayed the inevitable of further currency decline and default.

“Have any dollars, sir?”

The morning of the first 25% devaluation we were sitting on a cobblestone street sipping cappuccinos when an older gentleman popped out of an alley and walked up to all the coffee shop patrons asking for dollars. He was not a beggar — far from it — he was very well dressed. He was walking around the tourist town offering westerners a great exchange rate.

The next tuk-tuk drivers I saw also were quite insistent that I could pay in dollars. They weren’t part of a financial institution that is required to clear trade in dollars, they were individuals who preferred dollars (and often Euros) over any other currency.

This is why I have to laugh at Bitcoiners and goldbugs who think the dollar being the global reserve currency is a giant conspiracy theory they learned about on Youtube. Well before Bretton Woods the global financial community was rapidly adopting the dollar. Dollar adoption accelerated quickly in the 60s and 70s as the repo market was rapidly expanding and offshore dollar deposits (EuroDollars) around the world ballooned, causing the great inflation of the 60s and 70s.

The dollar was already becoming the global currency along with the British Pound. But during WW1, Europe became indebted to the US, and gold (the reserve currency of the time) flowed into the US. The US became the lowest credit risk and the most stable currency.

Central bankers have always positioned and lobbied to have their currency become an international one, but the EuroDollar system is a decentralized shadow banking system chosen by commercial bankers around the world.

The Global Dollar Shortage

The dollar (or “EuroDollar”) being the global reserve currency means that it is the “medium of exchange” for all global transactions. If Sri Lanka wants to buy something from China, they need dollars.

Again, when you can’t produce your own dollars via growth, you have to deplete reserves. All imports require dollars, and as discussed, everyone is dependent on imports for many essentials, including food.

As Sri Lanka depletes reserves and produces less, its central bank is both having to buy back the currency in order to maintain the “peg” and fund imports on its own… Which it can’t fund because GDP is down and they’re already in a deficit. They can only maintain this with more debt, which will then require more debt just to make the payments — a debt ponzi.

Sri Lanka had no “choice” when they devalued the currency, it’s the market’s price discovery.

Those in love with the “dollar flood” inflation narrative (and who don’t know what M2, QE or “bank reserves” are) have to explain why governments around the world are blaming a dollar scarcity.

India and Nepal

The next two countries we visited were also having rolling power outages that increased in length — India and Nepal. Despite the expectations of locals, by the end of our trip power was out all day everyday, at least in the rural areas where we stayed.

Famously, India has found relief by working with Russia to import oil at a discount. But when we got to Nepal they had begun more drastic measures than their previous 80% tariffs on cars — they decided to completely ban the import of cars.

“Nepal banned imports of cars, alcohol, tobacco and other luxury items Wednesday and shortened its work week to help conserve its dwindling supply of foreign exchange.”

Dollars. When they refer to “foreign exchange” reserves, they mean dollars. And when I say “dollars”, I mean dollar denominated assets, like treasury bills — “EuroDollars”. We don’t clear global trade in cash, instead financial institutions around the world need dollar denominated assets lent out and acquired in the repo market (why do you think the bank so wants you to refinance your mortgage?).

“… also forbids imports of toys, playing cards and diamonds. Without such drastic measures, the foreign currency reserves needed to import almost everything will last only a few more months, officials said.”

The article states that the cause of the reserve shortage is that Nepal relies on tourism and tourism is down. Currencies devalue not by choice but by the loss of productivity in the economy. However, central banks who have pegs first try to use debt instead of paying less for their currency repurchase. First they liquidate reserves.

More than a coincidence, central banks all over the world are liquidating their reserves as well. This is not unique to countries we travel to — this is a global dollar shortage.

Dollars are lent into existence by commercial banks (not the Fed) and are reliant upon growth for loans to be productive and for monetary expansion to continue. When loans are not productive, as we’re seeing, there is a shortage of bonds / collateral to clear trades. When dollar supply declines globally, imports globally have to decline.

Liquidity supply shocks

It’s fascinating that major dollar shortages (like 2008 and March 2020) are often (always?) preceded by liquidations of treasuries.

In 2020 treasury bills spiked with the 30 year going up almost 50%. However, right before that the Fed was in panic trying to buy treasuries up as they saw no one else was buying. Massive selling followed by a squeeze.

In 2008, when no one wanted commercial paper, mortgage backed assets and corporate bonds, financial institutions were all driven into treasury bills. JPM demanded that Lehman provide treasuries. The largest dollar shortage event of our era, yet it started with a mass liquidation of treasuries.

Right now, we’re seeing all the signs of a dollar shortage but treasuries are going down in value, and have been since before “rate hikes” were announced (the Fed tends to announce these rate adjustments after the market moves that way).

Jeff Snider recently wrote a piece talking about foreigners liquidating treasuries. Even the central banks of China and Japan are stepping into commercial markets to help their companies meet dollar bond obligations.

Snider calls the TIC data “chaotic” and liquidity in general seems chaotic. Dollar bond obligations are barely able to be met and it’s at the expense of central banks, and yet treasuries are being sold (and rebought). And by no coincidence, Chinese exports are declining.

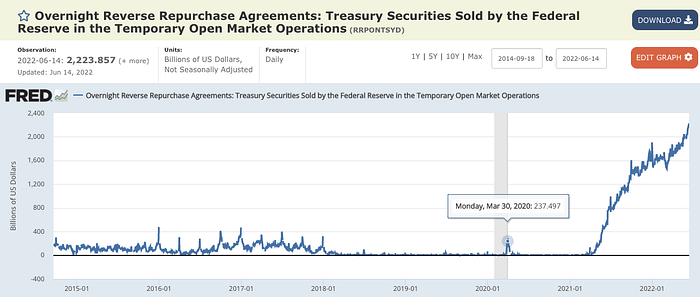

Similarly, the Fed’s reverse repo has hit yet another record, now $2.2 trillion a day. Despite the common narrative, the Fed’s RRP spikes in times of illiquidity like quarter ends and March 2020 (and its spikes are generally followed by lower Chinese exports). This current spike of $2 trillion is a real explosion over 7 times higher than March 2020, the second greatest dollar shortage event in the last decades according to the BIS.

Snider shows that even the central banks of China and Japan are liquidating dollar reserves. Specifically, they are liquidating US treasuries. China has been using its dollar reserves to make sure its giant near-bankrupt companies, like Evergrande, continue to make dollar bond payments.

Furthermore Snider shows that these movements in their bank reserves correlate with volatility in the Yuan and Yen.

Again, all major debt is in dollars. In order for China and Japan to create (and use) its own dollars, they lend in dollars. However, what happens when its companies, like Evergrande, stop being productive and can no longer produce their own dollars? They can go bankrupt or the central bank can liquidate their own reserves. What happens to China’s financial institutions that rely on these dollars and it’s lenders?

Taking on debt to solve a dollar problem works only if you can be more productive than before. Otherwise, you postpone a larger default. Yet, GDP growth has continued to slow globally as debt relative to GDP has risen. While I don’t think it’s a coincidence that debt grows and GDP growth slows, it’s certainly a bad combination. It means that the global economy has more and more resembled a debt ponzi, only making payments after raising more debt.

These dollar shortages start with desperate liquidations to meet dollar obligations. When dollar obligations aren’t met, the shortage becomes a crisis. Central banks all over the world are scrambling to meet bond obligations in fear of what happens when they fail. Default means too few EuroDollars to clear trade.

What happens to countries with central banks that have used all their dollar reserves and they aren’t producing any more dollars? Imports cease. This is incredibly concerning given the incredible dependence the globe has on imports from others. Consider that places like Fiji import over half their food. Malawi imports 75% of its food! What happens to their citizens when they can’t import?

A warning of the boom and bust of global debt

My wife and I first visited Sri Lanka exactly a decade ago and in many ways the growth has been incredible. Colombo, the capital, is in the midst of a Dubai-like creation of an entirely new city within the city — Colombo International Financial City (although I’m already skeptical of how sustainable anything “Dubai-like” could possibly be).

Despite the growth, I’ve never in all my travels had as many people tell me about their debt problems. And this wasn’t just in Sri Lanka, it was everywhere we went. People seem generally more desperate than ever before. In fact, we’ve gotten messages from people all over the world that we’ve met in previous travels during COVID asking for financial aid.

But I had already begun to notice the drastic increase in debt a few years before.

Revisiting a remote island elsewhere in Asia I realized the community had an explosion in new collateralizable assets, like homes and cars (EuroDollar creations of the monetary system). People who make in a day the equivalent of our hourly minimum wage were driving nicer cars than I had ever owned.

Remember the scene in the Big Short when Mark Baum (Steve Carrell’s character) and his team realize that strippers in Florida have 3 houses? My malinvestment radar is picking up a similar vibe.

Japan has historically run head first into copying the worst of Wall Street and now they’re recreating the easy dollar system that led to the financial crisis. They’ve become the EuroDollar creator and primary lender of dollars in Asia.

If people in small rural areas of Asia are able to have such liberal access to large amounts of debt, there is something seriously wrong with the due-diligence process of these loans and it indicates to me that it is done at a scale that is not sustainable.

The one conclusion Richard Vague gives in A Brief History of Doom: Two Hundred Years of Financial Crises (great book) is that the only predictor of financial crises is a sudden increase in debt. If there is a sustainable rate of lending, you can’t suddenly double it without default (which leads to a monetary shortage).

One particular story stands out from our Sri Lanka trip.

As mentioned, everywhere I went people lamented about their financial troubles. Even when we just stopped and got coffee from a hotel owner that had a little attached cafe in rural Nepal, we heard about how underwater this guy was on his loans. Even in the brief time it took to drink a coffee we heard about people’s debt burdens.

My wife noticed on the back of a menu in Sri Lanka how the restaurant was thanking special foreign patrons who had helped finance necessary repairs, renovations, loan payments, etc.

It’s just a feeling, but given the incredible persistence which we heard about people’s loans, one couldn’t help but feel these people were looking for more special patrons to help with their loans.

But the Big-Short-like moment of realization which I want to share was from a hotel in a remote area in the mountains of Sri Lanka. The owner was in the middle of building the hotel when he ran out of money. So there are more planned floors and no facade, but the rooms were nice enough.

There were 6 available rooms in this hotel maximum and half of them were full on a holiday weekend.

Talking to the owner one morning, who was actually quite pleasant, I repeatedly heard about his financial issues. However, this time I was quite intrigued when I found out that his loan was $7,000 a month!

What?!

We were paying $20 a night and even if all the rooms were sold out 30 days a month, and if he didn’t have to pay 15% to Expedia, and if he had no other expenses… that’s only half of the loan!

How was this guy ever able to pay his loan? Was he just refinancing and rolling over debt?

Furthermore, a bank supposedly gave a guy in a rural area with land, concrete and rebar, a $7,000 month loan. This isn’t a stripper in Florida with a $2,000 a month loan, this is someone in a rural area of a third world country.

While I can’t verify his $7,000 a month mortgage, I could see both his desperation and his half built hotel. And he wasn’t the first or last to complain of a heavy debt burden. The point is, regardless of the actual amount, in just a few months I met a lot of people underwater on their loans, and paying off a lesser amount.

I get the feeling that these are the same type of loans I’ve seen in other parts of Asia. At the time, I thought less of it. Perhaps they have to give back their new car, oh well. Now they seem unscrupulous.

The scary thought is 1) if all financial crises are debt crises, this one is even more over-lent than the mortgage crisis. And 2) if defaults on dollar denominated assets (like mortgages) lead to global financial crises because there’s already a shortage of dollar denominated collateral (hence yields declining for decades as dollar assets are bid up in value), this seems way more widespread, and even less due diligence, than subprimes in 2008. Japan’s lending to Asia is a major source of global EuroDollars.

History is clear that financial crises are also monetary shortages. In a fractional reserve system built on the back of commercial lending, when events like 2008 and 1929 happen, it isn’t just the defaults that lead to crisis, it is a shortage of dollars used as medium of exchange.

In the coming months/years watch how China’s exports (which are already getting more volatile at quarter end collateral illiquidity crunches), and everyone else’s imports, will be declining in sync with dollar collateral shortages. Dollars going up in value mean imports are more expensive and global trade is more expensive.

I predict this is not good for China, not good for Japan, not good for third world countries, not good for “pegged” currencies, not good for dwindling central bank reserves, not good for import countries, not good for corporations only surviving by rolling over debt (25% of all our public companies), not good for employment (lower rates are associated with lower labor force participation), and not good for those holding assets that appreciate on the back of debt expansion (like real estate).